How to Buy a House with No Money Down

Look, if you’re paying $3,000 a month in rent but can’t scrape together enough for a down payment, you’re not alone. That’s the trap most people find themselves in. You can afford the monthly payment, you just can’t get past that initial $15,000 to $30,000 hurdle while you’re already handing over three grand to your landlord every month. Compare renting vs buying to see the exact monthly costs.

There’s a no money down program through A Good Lender in California that solves this problem, and most first-time buyers have never heard of it. We cover your entire 3.5% FHA down payment on homes up to ~$863,000 (FHA route), or 3% on higher-priced homes using conventional financing. After you’ve lived in the house for six months, you never have to pay it back. Not three years, not five years. Six months and you’re done.

I’ve been doing mortgages in California for over 30 years. This is the fastest no down payment solution I’ve seen.

What Is California’s $0 Down Lender-Paid Grant?

We pay your 3.5% FHA down payment at closing. For FHA loans, the program caps at $832,750 loan amount (max sales price ~$863,000). Need to go higher? Use a conventional loan with 3% down, which goes up to your county’s conforming limit. It does not get recorded as a second mortgage on your property, but here’s the thing: you don’t make any payments on it. Zero. No monthly bill, no interest accruing. It just sits there quietly for six months. It’s truly $0 down from your pocket.

After 180 days, the whole thing gets forgiven provided your payments were made on time. You don’t pay it back. You don’t owe taxes on it. It’s just yours.

This is a lender-paid no down payment program, not a city or county government program. Compare that to other California financing options. CalHFA’s Forgivable Equity Builder makes you wait five years. Dream For All makes you pay back the money plus a chunk of your home’s appreciation when you sell. CalHFA MyHome? You have to pay the whole thing back eventually. Local city and county programs often have waitlists or lottery systems. This program is different. Six months and you’re completely done with it.

The only real requirements are that you work with A Good Lender, use it with an FHA loan, and actually live in the home for those six months. That’s the deal. Want to compare with other California assistance options?

Ready to See Your Numbers? Use our county calculator to find out exactly how much down payment assistance you qualify for. Takes 30 seconds. Check Your County Limits →

What Are the Program Limits by County (2026)?

This grant covers your full down payment. For FHA loans (3.5% down), the program caps at $832,750 loan amount regardless of county, which means a max sales price of ~$863,000 and max grant of ~$30,205. For higher-priced homes, use a conventional loan (3% down) up to your county’s conforming limit.

| Loan Type | Max Loan Amount | Max Sales Price | Max Grant |

|---|---|---|---|

| FHA (3.5% down) | $832,750 | $863,005 | $30,205 |

| Conventional - Standard Counties | $832,750 | $858,505 | $25,755 |

| Conventional - High-Cost Counties | $1,249,125 | $1,287,758 | $38,633 |

High-cost counties (Los Angeles, Orange, San Francisco, Alameda, etc.): Conforming limit $1,249,125 Mid-tier counties (San Diego $1,104,000, Monterey $994,750, Ventura $1,035,000) Standard counties (most Central Valley, rural): Conforming limit $832,750

Check your specific county’s limits at agoodlender.com/no-down-payment-program-in-california.

Who Qualifies for No Money Down Home Loans in California?

If you can qualify for an FHA loan or conventional loan, you can qualify for this program. That’s it.

There’s no special first-time buyer requirement, no income caps, no homebuyer education course for this no money down program. Standard mortgage qualification rules apply. Credit score, income verification, debt-to-income ratio. Same stuff we check for any home loan.

The main thing to know is the FHA route caps at $832,750 loan amount (max grant ~$30,205). For higher-priced homes, use a conventional loan—in high-cost counties like Los Angeles, Orange County, and Alameda, you can receive up to $38,633 (3% of $1,287,758 max sales price). Check your specific county’s limits at agoodlender.com/no-down-payment-program-in-california.

The other requirement is living in the home as your primary residence for at least six months. That’s when the assistance gets forgiven. After that, you can sell, refinance, or stay as long as you want.

How Does 0% Down Payment Assistance Work at Closing?

When you close on your home, we pay your down payment directly at the closing table. On a $450,000 purchase, that’s $15,750 showing up as a credit against your down payment requirement. You’re not making monthly payments on it. There’s no interest ticking away. It just sits there while you live in the home and make your regular FHA mortgage payments.

After 180 days, the whole thing gets automatically forgiven.

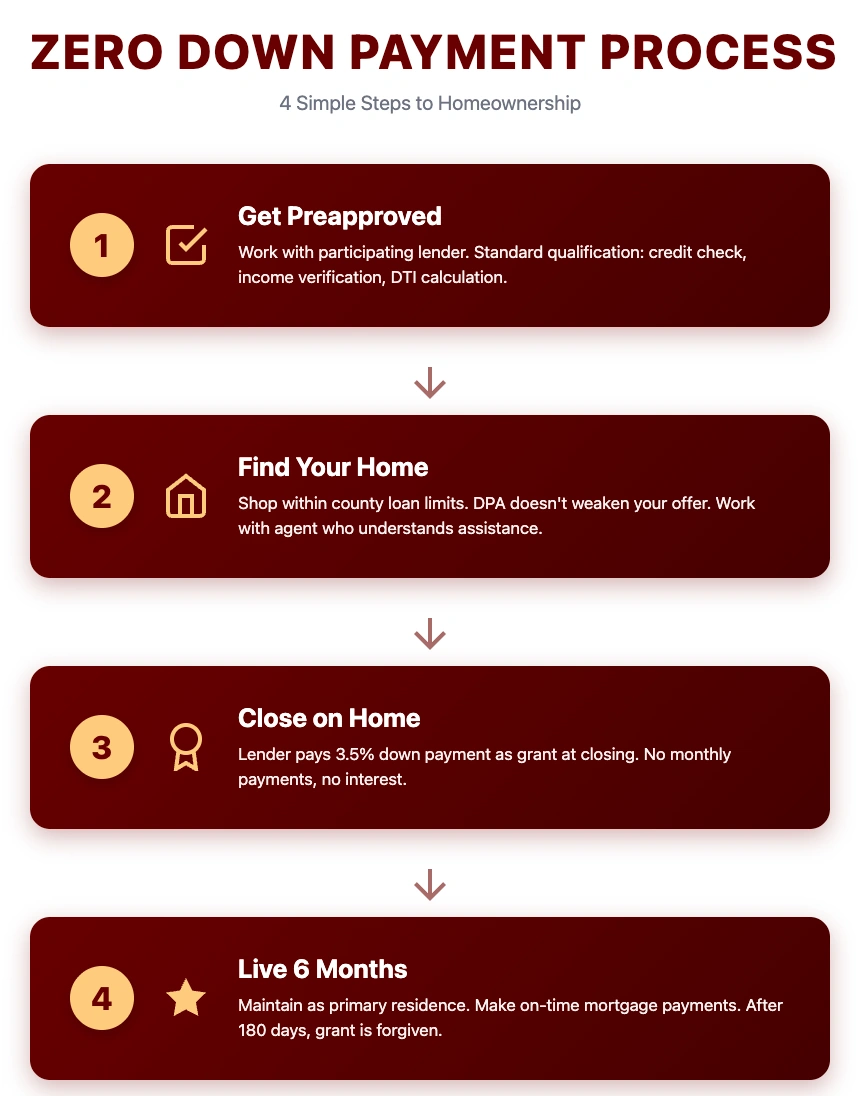

The complete zero down payment process: Get preapproved → Find your home → Close with A Good Lender assistance → Live 6 months for full grant forgiveness

What Is a Real Example: Buying a $450,000 Home with No Money Down in Sacramento?

Here’s an example with actual figures. Suppose you are buying a $450,000 house in Sacramento.

How Much Down Payment Is Required?

The down payment requirement with an FHA is 3.5%. This equates to $15,750. We pay all of this through this particular program. Your down payment? $0.

What Are the Costs?

With no down payment required, you still need closing costs, which typically run about $8,000 to $10,000. This is where you can get creative.

Strategy 1: Negotiate Seller Credits

The seller credits are quite significant. This is something you can negotiate up to 6% of the price, which, if you are buying a house costing $450,000, you can get $27,000. But what you can realistically get, and this will be ample to pay your closing costs of $10,000, is between 3% and 4% from the sellers.

Strategy 2: Use Family Gift Funds

So, if you have family members who can help, FHA permits gift money from family members. All you need is a gift letter. So, if your parents can afford to kick in $5,000, that already takes care of half your closing expenses.

Strategy 3: Accept Lender Credits

Another choice is lender credits. You take a small bump in interest rate, perhaps to 6.75% from 6.5%, and receive $3,000 to $5,000 in lender credits, which you can apply against your closing costs. This raises your monthly payment slightly, but you need less out-of-pocket money up-front.

How Do You Combine Strategies to Minimize Out-of-Pocket Costs for Zero Down?

People typically pay for things by mixing and matching these approaches. Maybe you receive seller credits to pay for most, then perhaps a small gift from family members. So you walk into closing with perhaps $3,000 to $5,000 out of pocket. And if you’ve already got that money in your savings and you’re already paying $2,800 a month rent, you can afford to purchase a house.

Calculate Your Zero Down Payment Scenario See exactly how much lender assistance you’d get for a home in your county. No signup required. Use Free Calculator →

Where Does No Money Down Assistance Work Best in California?

This program is available all over the state through A Good Lender, and it covers all counties in California.

How Does This Work in the Central Valley?

Fresno, Bakersfield, Stockton: Median price ranges from $350,000 to $500,000. Our contribution towards closing costs and assistance with your 3.5% down payment will apply to most homes in these areas.

How Does This Apply in Los Angeles?

Look at areas like San Fernando Valley, Inland Empire, East County San Diego where $400,000 to $550,000 homes are common. The full 3.5% down payment gets covered.

How Does This Work in the Bay Area?

Higher prices, but the program still covers your full down payment. On a $700,000 home in Orange County (within the FHA max of ~$863,000), we pay the full $24,500 down payment (3.5%). For homes above $863,000, use conventional financing with 3% down.

Next Steps to Get No Money Down Assistance in California

If you want to use this program, here’s what you actually need to do.

First, check your county’s loan limits. Go to agoodlender.com/no-down-payment-program-in-california and punch in your county. You’ll see your FHA limit, conventional limit, and how much down payment assistance you’re eligible for. Takes maybe 30 seconds.

Second, get preapproved with A Good Lender. We offer this program. You’ll need to provide income documentation, get your credit pulled, verify your employment. Standard preapproval process. The preapproval letter should specifically mention the down payment assistance so sellers and agents know you’re serious.

After that? Find a home, make an offer, close on it. We pay your down payment at closing. After six months, it’s completely forgiven. That’s the whole process.

If you’ve been stuck renting because you can’t save for a down payment while you’re paying $3,000 a month to your landlord, this no money down program is how you get out. Check your numbers and get moving.

Related Down Payment Assistance Programs

Looking for other ways to cover your down payment? California offers several additional programs worth exploring:

- Elite Grant in California - Private lender grant programs with 6-36 month rapid forgiveness

- CalHFA Programs - State-backed down payment assistance with 10-year forgiveness options

- Local DPA Programs - City and county government grants ($10K-$200K) from San Francisco, LA County, Orange County and more

- FHA Loans in California - Complete guide to FHA financing with low down payment requirements

- Physician Mortgage Loans in California - 100% financing with no PMI for physicians, dentists, pharmacists, and other medical professionals

- All Down Payment Assistance Programs → - Compare every option available in California