The neighborhood you pick gets most of the attention. But the type of home you buy shapes everything that happens at the mortgage desk. It determines which loans you can use, how much you need down, and how complicated your approval will be. This guide covers all 8 property types in California, what each one is, who it tends to fit, and the financing picture for each.

Here’s a snapshot before we break each one down:

| Home Type | Common Loan Types | Financing Complexity |

|---|---|---|

| Site-built single-family | Conventional, FHA, VA, USDA, Jumbo, CalHFA | Easy |

| Condo | Conventional, FHA (approved projects), VA, Jumbo | Moderate |

| Townhouse | Conventional, FHA, VA, CalHFA | Easy to Moderate |

| Co-op | Specialized share loans only | Complex |

| Multifamily (2-4 units) | Conventional, FHA, DSCR | Moderate |

| Manufactured home | Conventional, FHA, chattel | Moderate to Complex |

| Modular home | Conventional, FHA, VA, Construction-to-Perm | Easy |

| Tiny home | Personal loan, RV loan, limited mortgage | Complex |

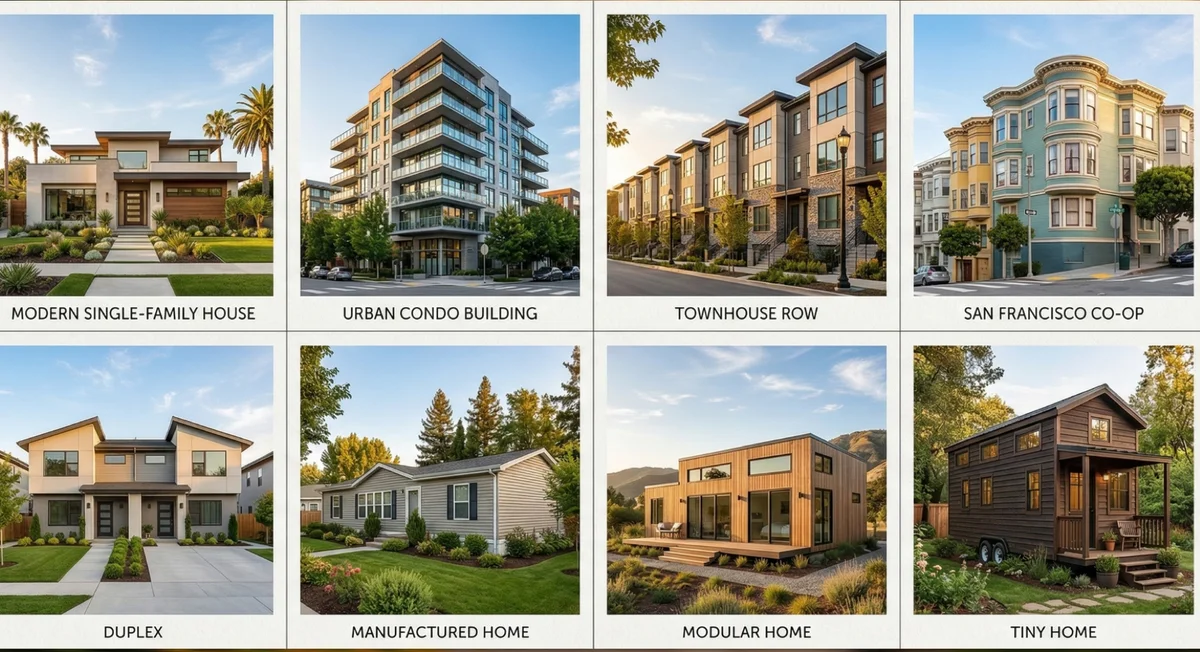

Site-Built, Detached Single-Family Homes

A site-built home is constructed on the property itself, from foundation to roof, designed for one household. There are no shared walls, no units above or below, and the owner controls the structure and the land subject to local zoning rules. This is the most common property type in California and the one most loan programs are built around.

No other property type gives you this many loan options. Conventional, FHA, VA, and USDA loans all work here with no extra approvals or eligibility hurdles tied to the property itself. Your qualification depends on your credit, income, and down payment, not on whether the property clears a project review. If you haven’t owned a home in the last three years, CalHFA programs can layer on top to cover the down payment entirely. See conforming loans in California, FHA loans, and how to buy with no money down.

Condominiums (Condos)

When you buy a condo, you own the interior of your unit and share ownership of common areas: hallways, landscaping, amenities. A condo association manages the exterior and shared spaces, and you pay monthly HOA dues to cover those costs. Condos tend to be more affordable entry points in expensive California markets like Los Angeles and San Diego.

Lenders split condos into two categories: warrantable and non-warrantable. A warrantable condo meets Fannie Mae and Freddie Mac requirements: owner-occupancy above 50%, no single entity owning more than 10% of units, and a financially stable HOA. Non-warrantable condos are harder to finance and typically require portfolio lenders with higher rates and stricter terms.

FHA and VA loans add another layer. Both programs require the condo project to appear on their approved list before you can use the loan. If the complex isn’t already approved, single-unit approval is possible in some cases but takes extra time. For first-time buyers, CalHFA programs can apply to FHA-approved condo projects and cover the down payment. See condo loans in California for a full breakdown.

Townhouses

A townhouse shares one or more walls with neighboring units but gives you ownership of the structure and the land beneath it. There are no units above or below, which is a key distinction from condo living. Maintenance responsibilities vary by HOA.

Most townhouse communities are classified as Planned Unit Developments (PUDs), which means lenders treat them like single-family homes for financing purposes. There’s no project approval requirement like there is with condos. Conventional, FHA, and VA loans all work here.

Lenders still review HOA documents during underwriting to confirm the association is adequately funded and not carrying pending special assessments. Your monthly HOA dues also factor into your debt-to-income (DTI) ratio, so they affect how much you can borrow. Factor that in before you start shopping. CalHFA programs apply to townhouses as well, so first-time buyers have a path to zero down here too. See conforming loans in California.

Co-ops (Cooperatives)

With a co-op, you don’t buy the unit itself. You buy shares in a corporation that owns the building, and those shares come with a proprietary lease giving you the right to occupy a specific unit. The co-op board holds approval rights over any buyer, so you’re not just being screened by a lender.

Co-ops are the most specialized financing situation on this list. Most conventional lenders won’t write a share loan because there’s no real property to secure the mortgage against. You need a lender who specifically works with co-op financing, and that narrows your options considerably. The board approval process adds time and uncertainty that standard mortgage programs aren’t built to handle.

One thing buyers often overlook: co-op monthly maintenance fees cover more than a standard HOA. They typically include the building’s underlying mortgage, property taxes for the entire building, utilities, and staff costs. That makes the actual monthly cash commitment higher than it appears when you’re comparing a co-op to a condo at the same price point. Co-ops are most common in San Francisco and a few other dense urban markets in California. See co-op loans in California.

Multifamily Homes

A multifamily property has two to four separate units under one roof: a duplex, triplex, or fourplex. One owner purchases the whole property and may live in one unit while renting the others, or buy it purely as an investment.

If you plan to live in one of the units, you can use a conventional or FHA loan. FHA allows as little as 3.5% down on a 2-4 unit owner-occupied property. The rental income from the other units can count toward your qualifying income, and most lenders allow 75% of projected rent to factor into your application.

Investors who won’t occupy the property take a different path. DSCR loans qualify based on what the property earns in rent rather than your personal income, which makes them well-suited for buyers building a small portfolio. See multifamily loans in California and DSCR loans for both scenarios.

Manufactured Homes

A manufactured home is built entirely in a factory, then transported to the site on a permanent steel chassis. To qualify for most mortgage programs, the home must meet HUD construction standards and must have been built after June 15, 1976, when those standards took effect.

With manufactured homes, the title is everything. If the home is on a permanent foundation and titled as real property, it can qualify for a conventional mortgage or FHA loan. If it’s still titled as personal property, you need a chattel loan, which works more like auto financing: shorter terms, higher rates, no government-backed programs.

Converting from personal property to real property is possible but involves a title conversion process that varies by California county. Understanding this before you make an offer can save a lot of complications during escrow. See manufactured home loans in California.

Modular Homes

A modular home is also factory-built, but it comes in sections and gets assembled on-site on a permanent foundation. Unlike manufactured homes, modular construction must meet local and state building codes, the same standards applied to traditional site-built homes.

Once a modular home is on its foundation, lenders treat it the same as any other site-built property. Conventional, FHA, and VA loans all apply, with no chattel complications and no title conversion concerns.

If you’re financing a new modular build rather than buying an existing one, you’ll need a construction-to-permanent loan to cover the build phase. A one-time close combines the construction loan and the permanent mortgage into a single transaction, which typically saves $3,000 to $8,000 in closing costs compared to closing twice. Rates on modular construction loans track closely with standard site-built construction financing. See modular home loans in California.

Tiny Homes

Tiny homes are typically under 400 square feet and can be built on a permanent foundation or designed to be movable. They appeal to buyers focused on lower costs, minimal upkeep, or flexibility in where they live.

Financing is the biggest obstacle. Most lenders have minimum loan amounts and minimum square footage requirements, often between 400 and 600 square feet, and tiny homes regularly fall short on both. If the home is on a permanent foundation and meets local building codes, some lenders will consider it. If it’s on wheels or registered as an RV, you’re looking at a personal loan or RV loan instead.

California zoning rules vary widely on where tiny homes can legally be placed. Research that before you commit to a property, because not every lot or community allows them.

If you’re still deciding between property types and want to know what you’d actually qualify for on each, call (510) 589-4096 before you start shopping. It changes what you look at.

Need Help with Your California Mortgage?

Whether you're buying, refinancing, or tapping equity, we've got 40 years of experience finding the right loan for your situation.

Frequently Asked Questions

Can I use an FHA loan to buy a condo in California?

Yes, but only if the condo project is FHA-approved. The FHA maintains a list of approved condo projects, and your unit must be in one of them. If the complex isn't approved, you can apply for single-unit approval, but not all projects qualify. Warrantable condos with strong HOA financials and low investor concentration are most likely to pass.

How are manufactured homes financed differently from regular homes?

The key factor is how the home is titled. If a manufactured home is on a permanent foundation and titled as real property, it can qualify for a conventional mortgage or FHA loan. If it's titled as personal property, it needs a chattel loan, which typically carries higher rates and shorter terms. Most lenders also require the home to be built after June 15, 1976, when HUD construction standards took effect.

What is the difference between a modular home and a manufactured home for financing?

A modular home is built in sections at a factory, then assembled on a permanent foundation on-site. It must meet local and state building codes, just like a site-built home. Lenders treat modular homes the same as traditional construction once they're on the foundation. Manufactured homes are built to federal HUD standards instead of local codes and sit on a chassis, which creates more financing restrictions.

Can I get a conventional loan on a co-op in California?

Most conventional lenders won't finance co-ops because you're buying shares in a corporation, not real property. Co-ops require specialized financing from lenders who work with share loans. The co-op board also has approval rights over buyers, which adds a step most mortgage lenders aren't set up for. Co-ops are most common in San Francisco and a few other dense urban markets in California.

How does buying a duplex affect my mortgage qualification?

If you plan to live in one unit of a 2-4 unit property, you can use rental income from the other units to help you qualify. Most lenders allow 75% of the projected rental income to count toward your qualifying income. FHA loans allow you to buy a duplex, triplex, or fourplex with as little as 3.5% down if you occupy one unit. The property still needs to appraise and the units need to be market-ready.

What financing options exist for tiny homes?

Tiny homes are the hardest property type to finance with a traditional mortgage. Most lenders have minimum loan amounts or minimum square footage requirements, and tiny homes often fall below both. If the home is on a permanent foundation and meets local building codes, some lenders will consider it. If it's on wheels or classified as a recreational vehicle, you're looking at a personal loan or RV loan, both of which carry higher rates than mortgages.